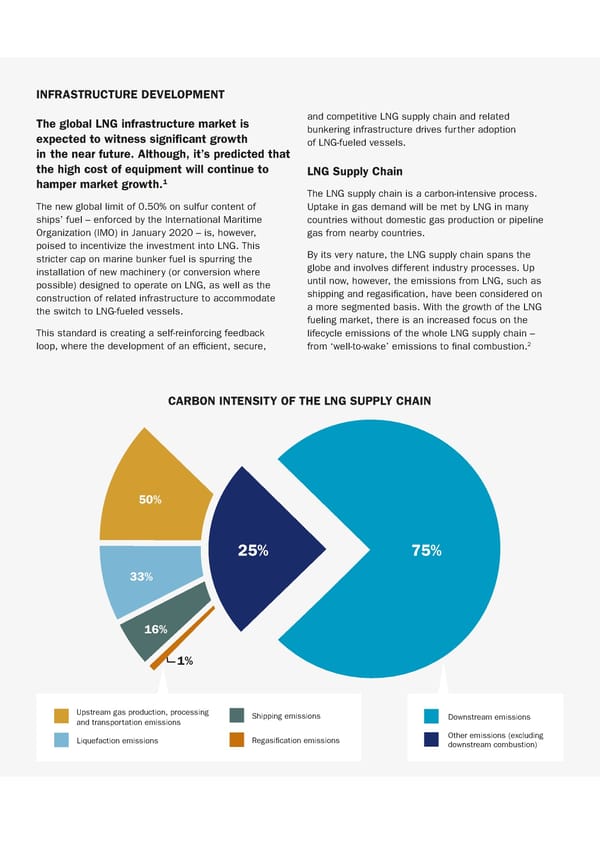

INFRASTRUCTURE DEVELOPMENT The global LNG infrastructure market is and competitive LNG supply chain and related expected to witness significant growth bunkering infrastructure drives further adoption of LNG-fueled vessels. in the near future. Although, it’s predicted that the high cost of equipment will continue to LNG Supply Chain hamper market growth.1 The LNG supply chain is a carbon-intensive process. The new global limit of 0.50% on sulfur content of Uptake in gas demand will be met by LNG in many ships’ fuel – enforced by the International Maritime countries without domestic gas production or pipeline Organization (IMO) in January 2020 – is, however, gas from nearby countries. poised to incentivize the investment into LNG. This By its very nature, the LNG supply chain spans the stricter cap on marine bunker fuel is spurring the globe and involves different industry processes. Up installation of new machinery (or conversion where until now, however, the emissions from LNG, such as possible) designed to operate on LNG, as well as the shipping and regasification, have been considered on construction of related infrastructure to accommodate a more segmented basis. With the growth of the LNG the switch to LNG-fueled vessels. fueling market, there is an increased focus on the This standard is creating a self-reinforcing feedback lifecycle emissions of the whole LNG supply chain – loop, where the development of an efficient, secure, 2 from ‘well-to-wake’ emissions to final combustion. CARBON INTENSITY OF THE LNG SUPPLY CHAIN 50% 25% 75% 33% 16% 1% Upstream gas production, processing Shipping emissions Downstream emissions and transportation emissions Liquefaction emissions Regasification emissions Other emissions (excluding downstream combustion)

TM&I LNG Flexibility Factor Report Page 4 Page 6

TM&I LNG Flexibility Factor Report Page 4 Page 6